David Beisel’s Perspective on Digital Change

Atomization of Seed Rounds Part I: An Explanation

When we first started NextView Ventures in 2010, we did so because we recognized that there was an underserved need for seed-stage capital particularly along the east coast between Boston and New York. And during that time, the venture market has evolved to a point where “Seed is the New Series A.” However, not only has the Seed round established itself as the first round of institutional capital prior to product-market fit, but recently it’s being smashed into pieces… into little atoms… the sizes and shapes of which each look and feel different from each other. Over a quick series of two posts, my plan is to explain of why this atomization is happening, share a roadmap for entrepreneurs and VCs to navigate this landscape in flux, and identify where I believe there are currently unique opportunities for founders, other VCs, and NextView.

My partner Rob Go previously wrote a detailed post on the reasons on why Seed has become the institutional venture capital financing prior to product-market fit. This dynamic has happened due to a number of converging trends: capital efficiency allowing founders to get further with less, some institutional seed rounds getting bigger, the bifurcation of seed VCs with some funds deliberately investing later while others going even earlier to do pre-seeds. In addition, Series As are getting bigger on average and very divergent overall. Most (but of course not all) internet-enabled startups typically raise some type of seed capital before eventually raising a round traditionally called a Series A.

But something else is happening which hasn’t been talked about as much. The Seed round itself has been fractured into smaller parts to be re-assembled in a bespoke fashion for each company.

Said another way, we’ve seen an atomization seed.

The cause of this trend sits at the intersection of two seemingly divergent factors:

- Increased startup capital efficiency means that founders can prove out early milestones – even important incremental ones – with small amounts of capital. It used to be that each step for increasing a startup’s value were large ones: an elephant-sized customer win, a monumental product shipment, or a huge new partnership. But now these value-steps have become more graduated: SaaS revenue building over time, progression along iterative product roadmap, or a string of API integrations. This series of small successive wins propels a startup forward continuously. Rather than a staircase of building value, the startup milestones have become an escalator.

- Series As are nearly all post-traction. When I started in venture a decade ago, Series A financings were much more about team, market, product vision… and often were before product-market fit and traction. Since that time, an influx of capital dedicated to the seed stage has entered into the market from angels, super-angels, seed funds, crowdfunding, etc. This situation has increased the number of seed-stage startups in the ecosystem, empowering traditional Series A firms to become more selective and require more proven traction before investing (along with a commensurately higher price for that de-risking). Today almost all Series As are post-product-market-fit and post-traction, with the intention of using that capital to fuel growth. Just five years ago, VCs were prescribing that “your next most important milestone [after a Series A financing] will be ship the product and get enough customers using the product to start to demonstrate evidence that you have product/market fit.” Fastforward to today, and even $100K in monthly recurring revenue for a SaaS business isn’t always a sufficient condition for raising a Series A round. The threshold for what constitutes a Series A ready company has shifted dramatically as traditional VC firms are requiring an increasingly greater level of traction.

Here is what happens at the intersection of these two realities: At the very same time, entrepreneurs can do more with less capital but are also required to do more to raise it.

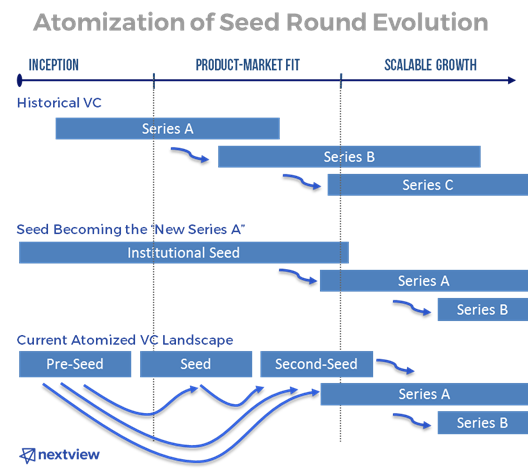

This confluence has resulted in entrepreneurs choosing (and sometimes being forced to) raise incremental stages of seed capital to successfully cross the Series A threshold. Raise a pre-seed round then a second-seed round, or raise an institutional seed round then a seed extension, or raise a series of incremental notes at higher implied valuations, or follow some other path entirely.

The graph below illustrates what has been and is now happening. In short, the startup path towards a Series A is no longer a linear one.

Some might lament this situation as a glut of seed-stage startups floundering towards crossing the Series A threshold which will result in a bloodbath of companies that fail to make the journey. But that characterization is simply not the case. In my next post, I’ll walk through the opportunities for entrepreneurs and VCs given this current dynamic.