David Beisel’s Perspective on Digital Change

The Shape of Traction (Part II: How Much Traction Do I Need to Raise a Round of Financing?)

A couple weeks ago, my partner Rob penned a blog post about the “shape of traction” which really resonated with a number of folks. The quick summary is that the shape of a startup’s traction (with time/product-quality on the x axis and traction on the y axis) and isn’t at all a linear path. Rather, when true product-market fit (PMF) happens, it’s an accelerating curve… and a very steep one at that! It will become extremely apparent to entrepreneurs (and investors) when it’s happening, so that if you have to ask where you are on the curve, it’s likely a signal that the startup isn’t on the right trajectory. Go read his post here.

The resulting question which my partners and I often hear in this context (and was asked for in the comments) is then: “How much traction do I need to raise a round of financing?” What are the actual numerical metrics which we need to demonstrate? The idea is that once you know the magic number(s), all a company has to do is work backward to accomplish that target goal. This rationale sounds rational, but the challenge with this logical goal-centric approach to metrics is that it’s based on the flawed assumption that the absolute scale of a startup is paramount when relative growth is often more important.

In other words, there are three important points about the shape of traction:

- Contour of the traction curve matters more than the absolute y-axis metric.

- Ability to extrapolate is key.

- Traction is graded on a curve, just like in high school.

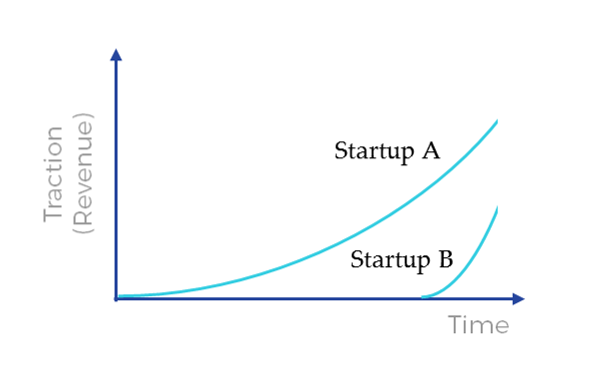

First, the contour. To illustrate with a simple example, take Startup A which takes five years to reach $200K in monthly revenue and compare it to Startup B which took one year to reach $100K in monthly revenue. On absolute terms, Startup A is twice as large. But Startup B is growing faster and likely that much more attractive for a venture investor at the Series A stage. The reason that the above is true is that investors build mental models about the ability of a company to continue with the same level traction moving forward. And therefore, many questions in evaluating a company are often diligencing if the progress made to date was repeatable, sustainable, and extensible. The idea is to ensure that there isn’t a natural ceiling approaching because a founder merely used brute force to demonstrate progress, but rather that the market is pulling current product (including all of its flaws) forward.

The reason that the above is true is that investors build mental models about the ability of a company to continue with the same level traction moving forward. And therefore, many questions in evaluating a company are often diligencing if the progress made to date was repeatable, sustainable, and extensible. The idea is to ensure that there isn’t a natural ceiling approaching because a founder merely used brute force to demonstrate progress, but rather that the market is pulling current product (including all of its flaws) forward.

The last main point is that traction is graded on a curve. How much was the startup able to accomplish given the resources that the company possessed to date? At the extreme end, if the company started as a side project and has been starved of attention, then it will be viewed differently than a company which raised a significant (pre-)seed round and hired a senior team to execute. Again, a VC investor is trying to suss out if the market is inherently pulling the success forward or if the team is merely pushing it. Eventually, even with a supremely exceptional team, the muscle runs out of energy without tailwinds of the market.

The takeaways for entrepreneurs given the perspective that VC investors have on the shape of traction:

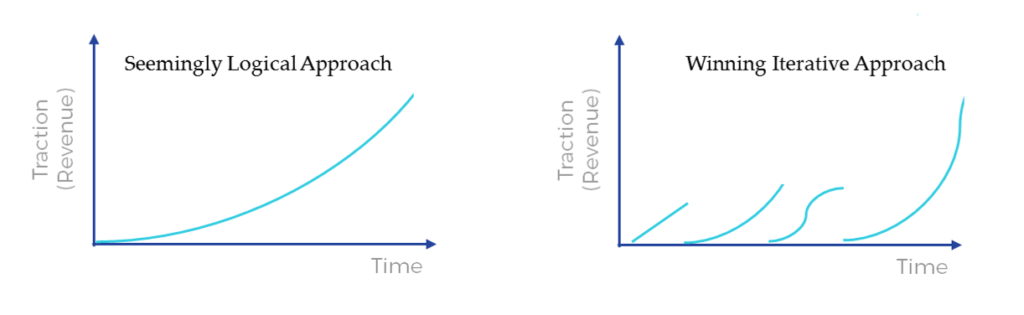

- The optimal approach to seeking product-market fit is for startups to initiate (and subsequently stop) a series of related experiments (so learnings from each one inform the next) until you find yourself on one with a very steep curve. The aim is to find a traction curve which is naturally steep, not push the existing curve upwards. A straight-line logical approach to won’t yield success as often as an iterative one.

- When positioning the company investors, tell a story about how the market is pulling you in a direction, and the company to date has been able to succeed with relatively little resources… with even more capital, the natural traction will continue.

The easiest to way to convince investors of traction is if you’re actually convinced of it yourself, which probably means you’re actually on the PMF curve. The right question to be asking then isn’t “How much traction do I need to raise a round?” but rather “how can I quickly iterate faster to find product-market fit?”